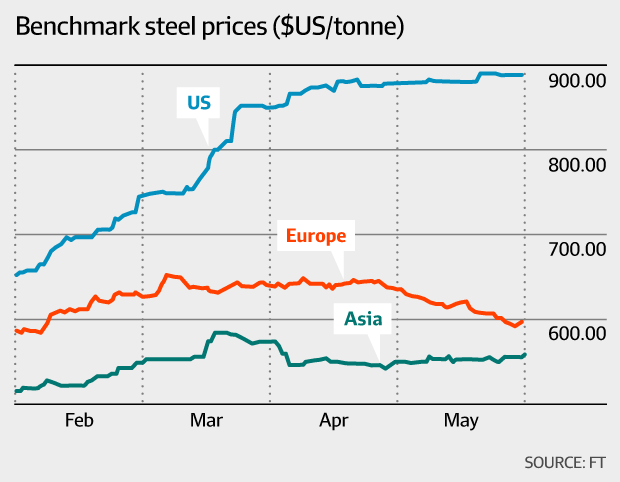

Donald Trump’s trade war carries a winner’s curseShare via EmailShare on Google PlusPost on facebook wallShare on twitterPost to LinkedinShare on Reddit The EU's retaliatory tariffs have prompted Harley-Davidson to move production for the European market out of the US. David Paul Morrisby Martin Sandbu The EU's retaliatory tariffs have prompted Harley-Davidson to move production for the European market out of the US. David Paul Morrisby Martin SandbuThe first shots in US president Donald Trump's trade wars ("good and easy to win") have been fired. Who is most likely to be hurt? And, in particular, were some of us right to say when Trump first started rattling his sabre that it would soon become clear that those bent on protectionism face high costs from turning words into action? Quite right, it seems. The story of the week is how the EU's retaliatory tariffs — which Brussels introduced in response to Trump's tariffs on steel and aluminium imports from Europe — has prompted Harley-Davidson to move production for the European market out of the US to avoid import duties it says will add $US2,200 to the cost of each motorcycle. It is not the only example of domestic casualties from Trump's trade aggression. It is important to understand that this is not just a matter of the EU lashing out in revenge. That would fit Trump's narrative and he could, with some justification, argue that the US can give harder than it gets, hence it stands to "win". But retaliatory import duties are just one of three ways Americans are hurt by their president's protectionism. There is also the higher cost of steel and aluminium he has engineered, which hits the bottom line of Harley-Davidson and other metals-consuming industries directly. (The US industries that use steel and aluminium as an input must be much more productive than those that produce the metal — that is why steel and aluminium producers want protection — so the tariffs hurt the things Americans are relatively good at to make them do more of what they are relatively bad at.)  The higher cost of steel and aluminium hits the bottom line of Harley-Davidson and other metals-consuming industries directly. The higher cost of steel and aluminium hits the bottom line of Harley-Davidson and other metals-consuming industries directly.Finally, and least well understood, if other countries lower trade barriers between them in a liberalisation that does not include the US, American exporters become less competitive in those markets. That is what is happening. For example: Japanese motorcycles, the EU import duty on which is being eliminated, now stand to gain market share from American ones. Meanwhile, the EU has just published its negotiation directives for the talks on liberalising trade with Australia and New Zealand. Perhaps Harley-Davidson should reconsider a decision to close its Australian plant. Advertisement[iframe][/iframe]What about China? It is playing the tariff game too — note how it is reducing tariffs on soyabean imports from Asian trading partners while raising them on US supplies — but it is less well positioned at it. That is because it imports so much less than it exports, and it is unwilling to undertake the sort of domestic reforms and policy commitments that would be required for free trade agreements with large economies. Brad Setser has looked at what else China can do to make Americans suffer from Trump's trade war against it. Focusing mostly on the threat to sell off Beijing's huge stake of US government bonds, he concludes that the answer is "not so much". As he correctly points out, the Federal Reserve could easily buy whatever stock of bonds China decides to sell so as to keep interest rates moderate. That is not the end of the story, however. If China shifts its holdings from low-paying bonds to higher-yielding assets, or pursues a policy of not to finance the US economy at all, then the American economy will need to pay more to finance its current account deficit, or run down its international investment position. Such a dent in the American "exorbitant privilege" of guaranteed cheap external borrowing rates could easily be self-reinforcing in that others will demand a higher yield for holding US assets. If this leads to a fall in the dollar and smaller deficit, that could be sustained and might just be in line with what Trump sees as desirable. But his government is not about to tighten its belt, so it would have to be the private sector doing so. That means either less investment by companies or lower consumption for households. There is a broader theme here. Trump may conclude from the fallout of the trade war that tariffs work as intended. If the EU's retaliatory duties can make Harley-Davidson move production out of the US, surely Trump's own protectionism can make other production move in. And his supporters, for now, seem to agree. The explicit goal of some of the president's advisers is to repatriate supply chains. They — and Trump, and his supporters — may think a world in which each economy (at least each large economy) produces mostly for its own domestic market would be a better one than the interdependent global economy we have now.  The Federal Reserve could easily buy whatever stock of bonds China decides to sell so as to keep interest rates moderate. The Federal Reserve could easily buy whatever stock of bonds China decides to sell so as to keep interest rates moderate.Until, that is, they see the cost. The rise of global production chains has transformed the nature of trade since the 1980s. For good reason: continental or global-scale production is more efficient than national-scale. The upshot is to be careful what you wish for. If Trump achieves a self-sufficient US economy, it would be a much less productive American economy (than it could be, and than its rivals). That would mean squeezed living standards, an increasing awareness of falling behind global leaders and a less harmonious society that squabbles over how to divide a smaller pie. In the end even his voters might get tired of so much winning. 本文为英国金融时报收费帖,找不到免费中文帖。以原文帖满足读者原阅读此文者。

|

雷达卡

雷达卡

发表于 2018-6-29 12:19:48

发表于 2018-6-29 12:19:48

QQ好友和群

QQ好友和群 QQ空间

QQ空间 腾讯微博

腾讯微博 腾讯朋友

腾讯朋友 微信

微信 收藏

收藏 分享

分享 提升卡

提升卡 置顶卡

置顶卡 沉默卡

沉默卡 喧嚣卡

喧嚣卡 变色卡

变色卡 千斤顶

千斤顶 照妖镜

照妖镜